We grants shares to the staff with vesting period accordingly. In between the grant date and vesting date, we account for the accelerated amortization under FRS When the staff resigned before the vesting date, it means the shares get forfeited. Does that mean we have to reverse the amount accounted for under the accelerated amortization previously booked for this shares, right? Hi Silvia. Hi Silvia, Given that a 5-year-life options were granted, b these options would become totally vested at 4th anniversary, c there is accelerated vesting clause which requires for more than 15 trading days within any consecutive 30 trading days in the Measurement Period e.

Or non-market vesting condition? Is the aggregative Target i AND ii a market condition?

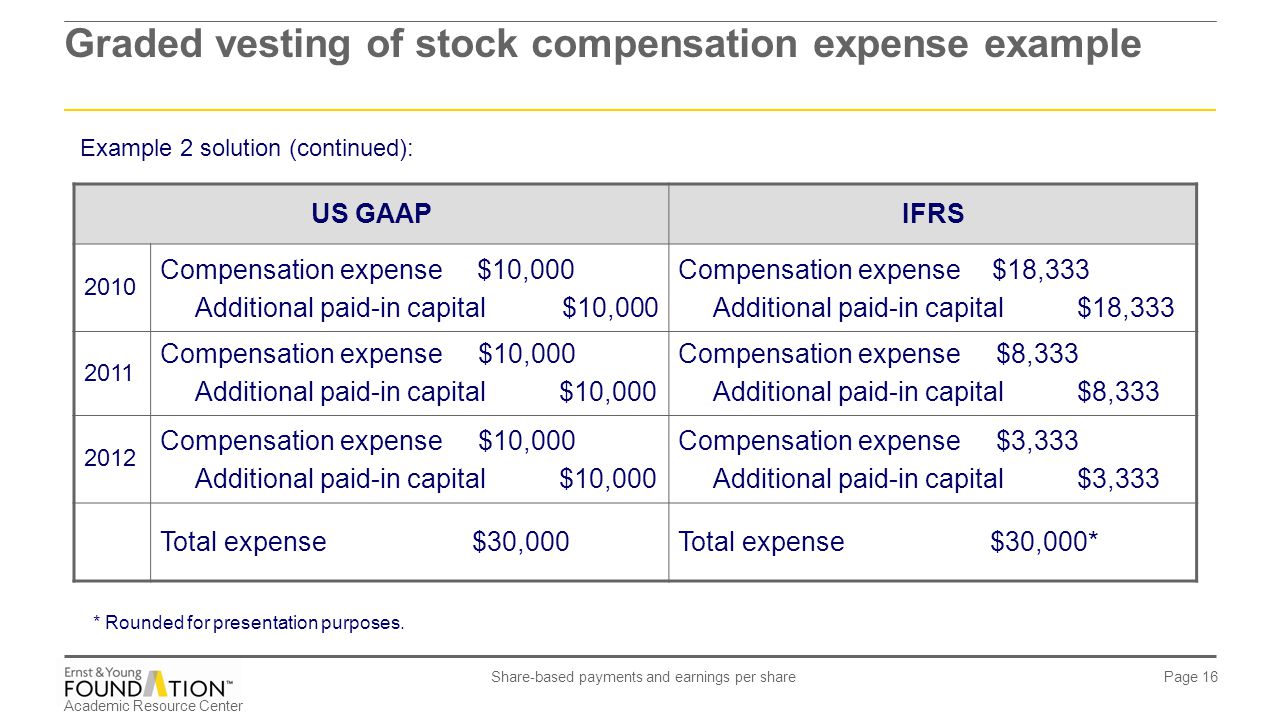

Share-based Payment (IFRS 2)

Under IFRS 2, should any market condition be considered in estimating share option expense? If IFRS 2 requires considering accelerating vesting clause, what is the period for amortization of option expense? Is it from grant date to the start of Measurement Period? If the Company has a mandatory convertible loan with fix interest rate per annum, and the principal and interest at the maturity date, will be converted in shares with fix to fix term.

Hi Silvia Thanks for the useful article. I have a question If employees of subsidiary company through monthly payroll deductions purchase the shares of parent company. The subsidiary books only a payable to parent company. Is this treatment correct? Or does IFRS 2 applied to the subsidiary company? I would like to have your input in a scenario where the company has granted share option to the employee with only one market condition that is the increase in share price with indefinite period. Whenever the condition is met the options will be vested. How are we going to treat this when there is no service period tied with this condition?

Regards, Ali. Dear Silvia, Thanks a lot for this very useful and informative article. This great, thanks and keep helping us understand the IFRS and become experts like yourself. Silvia, first of all thanks a lot for doing this — your articles are very useful and on several occasions I found these more understandable than guidance provided by big4 companies. IFRS2 says that equity-settled share-based payments should go to expense and increase in equity, but it is not really specified where exactly in equity is should be.

Recognition of equity-settled share-based payment transactions

Usually, it is going to separate reserve within equity — called Share-based-payment reserve or similar, which seems to be the best practice. But have you ever seen companies presenting equity-settled share-based payments in other section of equity — e. By using our website, you agree to the use of our cookies. Learn more Got it! Why IFRS 2? And what happens in such a case?

What is the objective of IFRS 2? Special For You! Click here to check it out! Check your inbox or spam folder now to confirm your subscription. Suthasinee Nimitkul February 27, at pm All articles of IFRSbox is very useful , easy to understand and presnted in a very constuctive way. Silvia M. February 27, at pm Thank you! I really appreciate your feedback! Snowia May 31, at pm Dear Silvia, These two points are confusing me.

This type of arrangement is cash-settled share-based payment transaction The key principle in IFRS 2 is to measure the amount of transaction at fair value of the goods or services received. June 2, at am Hi Snowia, please could you rearrange your question? Fawas December 23, at am Hi Silvia, Thank you very much for this.

One quick question. Hull January 8, at am This is such a great website. Saurav June 12, at am Hi Silvia, Thanks for such a simple explanation. Faisal January 19, at pm Salvia but FV of anything is the amount paid or received. January 19, at pm I simply disagree with it. June 29, at am Hiras, IFRS 2 does not apply to transactions with employees purely in their capacity as shareholders.

Mimie Fuerte July 14, at am This is very helpful! Kirsty August 18, at pm Hi Silvia, Thank you very much for your articles, always presented in the most simplistic way.

- how to trade gold options in mcx?

- IFRS 2 Share-Based Payment.

- What is the objective of IFRS 2??

May thanks Kirsty. Raja Wahab December 10, at pm Hello, I have a question. When a parent grants an option to its equity instruments to the employees of its subsidiary the subsidiary will treat it as an equity settled share based payment transaction as the liability of the award rests with the parent and will record the following entry: Dr Expense Cr Equity with fair value of the options vested or estimated to vest the parent will also treat the transaction as equity settled share based payment transaction and will recognise the fair value of options vested in its equity. Faisal January 19, at pm Hi Silvia, I have seen it for the first time its a good website.

April 27, at am Hi Chhaya, thank you! Ziafat Satti May 30, at am Hi, Thanks for sharing useful information. Please clarify. Ziafat Satti Auditor PwC. May 30, at am Dear Ziafat, are you sure that this transaction is a share-based payment? Ziafat Satti June 3, at am Yes it is a share based payment. Definitely buyer will be paying how IFRS does not apply? June 3, at am Oh, I see now. Ziafat Satti June 3, at pm Suppose a plant is acquired with fair value of cu 50 million, value of liability at acquisition date calculated based on share based is: 1. Cu 48 million What would be treatment of differencs in above cases at the trane date.

Asad October 20, at pm Do we take impact of favorable modifications in the option scheme if a performance market condition is attached or is it only for non market performance and service condition. October 28, at am Hi Asad, you did not give me enough information on this one. Can you be more precise? November 29, at pm Dear Sharon, in the case of employees, the fair value of services received is not readily determinable in most cases. Asmeeta February 26, at pm Thank you, Sylvia for the explicit article.

Meenakshi April 7, at am Hi Silvia, Above article is fabulous and well explained. Idotenyin October 3, at am i need practical question on share based settlement. Thank you.

Haris November 19, at pm Sylvia in recognition criteria you mentioned that when goods or services received shall be recognised as expense unless they qualify to be recognised as assets what does that mean. Haris November 19, at pm Your articles are very informative and easy to understand keep it up your good work. Johan Uys November 22, at am If the share scheme is classified as equity settled on a group level, but cash settled on a subsidiary level, what will the journals between the group and subsidiary be?

Syed Ali April 4, at pm Hi Silivia, After a vasting period how the cash and share based payment should be settled in Accounts what entries should we make. Johan Uys June 8, at pm If an employee receives an award that vests in 3 years which contains both a market and nonmarket condition, will you have to calculate 2 fair values and effectively treat it as two separate awards? Raymond June 15, at am If options are exercised, do we need to Debit Share based reserve and credit shares capital relating to those options exercised.

IFRS 2 — Share-based Payment

Sivani M July 28, at pm Could you please tell me what account will be debited when shares are issued to promoters for their services to company. Waqas Azeem May 27, at pm Hi dear, Your efforts are highly appreciated! In order to receive shares, employees must still be employed by Entity A at 31 December 20X2.

- IFRS 2 Share-based Payment;

- forex android trading system?

- IFRS 2 Share-Based Payment - CPDbox - Making IFRS Easy.

The fact that the market vesting condition i. It was taken into account when estimating the fair value of share options at grant date.

Their fair value is not subsequently remeasured after grant date. Non-vesting conditions are treated similarly to market vesting conditions , i. Interestingly, IFRS 2 does not give a definition of a non-vesting condition. However, it can be found in IFRS 2. BC non-vesting condition is any condition that does not determine whether the entity receives the services that entitle the counterparty to receive cash, other assets or equity instruments of the entity under a share-based payment arrangement.

Examples of non-vesting conditions are: target based on a commodity index, specified payments towards a savings plan during vesting period, continuation of the plan by the entity, non-compete clause, transfer restrictions. Modifications, cancellations and settlements are dealt with in paragraphs IFRS 2. In general, the cumulative expenses recognised with respect to equity settled share-based payment transactions after modifications, cancellations or settlements cannot be lower than before those events.

In other words, entities can only increase expenses and this will happen if modifications, cancellations and settlements are beneficial to employees or other party. If a modification increases the fair value of equity instruments granted measured immediately before and after the modification, number of these instruments, or both including replacement of old instruments with new ones , increased expense is recognised during the remaining vesting period in addition to the original expense. If the modification occurs after the vesting date, additional expense is recognised immediately.

A change in vesting conditions favourable to employees or other party should be accounted for as a revision to number of instruments that will vest. If the change relates to market conditions, it should be accounted as a change in fair value of instruments granted described above. A decrease in fair value of instruments granted including replacement of old instruments with new ones or unfavourable change in vesting conditions should be ignored and entity should recognise expenses based on conditions before the modification.